2026年6月23日

2026年6月23日

$5.5 Million Jump in 7 Months! This Type of Bulk Carrier Price is Soaring!

Recently, a transaction in the dry bulk secondhand market has drawn high attention to Ultramax asset prices. It is reported that the Dominator, a 64,000 dwt Ultramax bulk carrier built in 2021 at Shin Kasado in Japan, was reportedly sold for approximately $38 million. However, its sister vessel, the CMB Bruegel, was sold for $32.5 million in October 2025. In just about 7 months, the price of a similar type, Japanese-built, modern Ultramax has increased by roughly $5.5 million, a rise of nearly 17%. Additionally, in March of this year, the Ability, another vessel of the same age and size built by Shin Kurushima, was also sold for about $37 million, further confirming that modern Japanese-built Ultramax asset prices are rapidly rising. Analyst Liu Qingzhi from BRS pointed out in the latest weekly report that, according to Baltic Exchange valuation data, since February this year, secondhand prices for 5-year-old Ultramax vessels have surpassed the prices of newbuildings of the same type. As of the time of the report's writing, this premium had expanded to about 6% and continues to grow. Second-hand Ships are More Expensive Than Newbuildings BRS data shows that in the first four months of this year, the price of a 5-year-old Ultramax increased by 13.2%, reaching approximately $36.2 million; the price of a 10-year-old Ultramax increased by 15.8%, reaching approximately $28.6 million. Meanwhile, prices for Ultramax vessels aged 15 years and older remained firm, rising 9% in the first four months of this year. Even more noteworthy, the price gap between 5-year-old and 10-year-old Ultramax vessels has narrowed from 26% in 2025 to 20%. This indicates that the price increase is not limited to a few of the newest, highest-quality vessels, but rather the entire secondhand Ultramax asset curve is being pushed higher. Reasons for the Price Inversion...

2026年6月23日

2026年6月23日

Chinese construction + Chinese power! First batch of ethanol triple-fuel giant vessels in the world signed

The shipping industry's decarbonization transition has achieved a milestone breakthrough. Mining giant Vale, in partnership with Shandong Shipping, is building the world's first ethanol triple-fuel very large ore carriers (VLOCs). Vale announced that it has signed a contract of affreightment with Shandong Shipping Corporation for a new series of ethanol/methanol triple-fuel Guaibamax-class VLOCs. The new vessels will be built by Qingdao Beihai Shipbuilding Co., Ltd. (a subsidiary of China State Shipbuilding Corporation), with the main engine developed by China Shipbuilding Power Group Co., Ltd. Deliveries are scheduled to commence in 2029. This agreement sets an unprecedented milestone for global iron ore shipping: it marks the first time ethanol will be used as a primary fuel for ocean-going vessels. Compared to the conventional marine fuel oil commonly used in the shipping industry, the use of ethanol is expected to reduce greenhouse gas emissions by approximately 90%. This move reinforces Vale's commitment to reducing carbon emissions across its entire value chain and promoting maritime decarbonization, aligning with ongoing discussions at the International Maritime Organization (IMO). The 25-year contract of affreightment involves the construction of two new second-generation Guaibamax-class vessels, with options to build additional ships. The second-generation Guaibamax-class vessels measure 340 meters in length and have a deadweight capacity of 325,000 tons. Adopting this vessel type is part of Vale's multi-fuel strategy. These ships can use ethanol, methanol, or marine fuel oil as fuel, and their design also allows for future retrofitting to use liquefied natural gas (LNG) or ammonia as fuel. In addition to the triple-fuel design, the vessels will be equipped, like Vale's previously ordered second-generation dual-fuel Guaibamax-class VLOCs, with five rotor sails to harness wind energy and reduce fuel consumption. They will also feature several energy-efficiency improvements, including more efficient main engines, hydrodynamic energy-saving devices, shaft generators, variable frequency inverters,...

2026年6月23日

2026年6月23日

Six major shipbuilding companies join forces! The shipbuilding industry advances the development of a carbon emission accounting system.

Recently, the Korea Ministry of Climate and Environment (tentative name; official name: Ministry of Environment) signed a "Business Agreement on Assistance for Calculating Greenhouse Gas Scope 3 Emissions in the Shipbuilding Industry" with six major shipbuilders: HD Korea Shipbuilding & Offshore Engineering, HD Hyundai Heavy Industries, HD Hyundai Samho, Samsung Heavy Industries, K Shipbuilding, and Hanwha Ocean, at the Korea Chamber of Commerce and Industry (KCCI). The Korean government has united leading domestic shipbuilders to systematically calculate and manage greenhouse gas emissions generated across the entire value chain of the shipbuilding industry, aiming to establish an institutional foundation for reducing emissions. Greenhouse gas emissions are generally categorized into three scopes under the GHG Protocol based on measurement scope: Scope 1 (direct emissions): Emissions from sources directly owned or controlled by an enterprise/organization. Scope 2 (indirect emissions): Indirect emissions from the generation of purchased electricity, heat, steam, or cooling. Scope 3 (other indirect emissions, also known as carbon footprint): Other indirect emissions in the value chain not covered by Scope 2, including upstream and downstream activities. Given that the shipbuilding industry is closely linked to various upstream and downstream sectors such as steel, equipment, logistics, and transportation, the Ministry and the shipbuilding industry plan to first establish a calculation basis for Scope 3 that reflects the characteristics of the shipbuilding industry, and build an effective management system applicable to industrial sites. Under this agreement, the six major shipbuilders will, based on supply chain characteristics, emission scope classification, and data availability, study, analyze, and calculate the data and methods required for major greenhouse gas emission sources. Additionally, they will collaborate with the Korea Environmental Industry & Technology Institute (KEITI), an official agency under the Ministry, to develop plans to enhance on-site applicability. The Ministry plans to gradually expand the Scope 3 emission calculation assistance program...

2026年6月23日

2026年6月23日

Boosting Local Employment: Haizhongzhou Contributes to Regional Economic Development

As an industrial enterprise above the designated size that has been based in Duigougang Town, Guannan County for over a decade, Jiangsu Haizhongzhou Shipping Industry Co., Ltd. continues to generate social benefits in terms of employment promotion and local welfare, alongside its economic contributions. The company currently has approximately 2,500 production employees, about 70% of whom are local residents from Guannan County and surrounding towns and villages—including Duigougang Town, Tianlou Town, Changmao Town, and parts of Xiangshui County. For many local workers, being employed at the shipyard means they can balance income and family life without having to seek jobs in southern Jiangsu or other provinces. In terms of job structure, the company offers a wide range of positions, including welders, fitters, riggers, grinders, painters, pipefitters, electricians, mechanics, warehouse keepers, quality inspectors, and safety officers, with clear tiers of educational and skill requirements. New hires without prior shipbuilding experience can learn on the job through an "old-with-new" mentoring system, gradually taking up positions after short-term hands-on training. For skilled workers holding special trade certificates, the company provides skill allowances to encourage professional development. A small supporting service ecosystem has gradually formed around the company's premises. Small restaurants, convenience stores, breakfast stalls, hardware shops, and e-bike repair shops have opened near the factory gate, providing daily conveniences for employees while creating dozens of small business job opportunities. In addition, the company outsources logistics each year, commissioning local transport teams to haul steel plates, pipes, equipment, and hull sections, indirectly supporting nearly 100 transport-related jobs. In the area of talent development, the company actively cooperates with vocational schools in Lianyungang City and surrounding areas, including Guannan Secondary Vocational School and Lianyungang Vocational Technical College of Industry and Trade. Each year, the company receives interns majoring in welding technology, marine mechanical equipment, mechatronics,...

2026年6月23日

2026年6月23日

World's first "Far-Sea Floating Island"! Construction of major national science and technology infrastructure has commenced.

On March 27, the Shanghai Jiao Tong University Institute of Deep-Sea Science and Engineering was officially established, marking the full launch of the construction of the national major science and technology infrastructure project — the All-Weather Stationary Floating Research Facility in Deep-Sea Areas (a major scientific facility). This world-first, super-large offshore scientific research platform can simultaneously accommodate research needs in marine equipment, marine resources, and marine science, and is also known as the "Far-Sea Floating Island." Gong Zheng, Deputy Secretary of the Shanghai Municipal Committee and Mayor of Shanghai, together with Ding Kuiling, President of Shanghai Jiao Tong University and academician of the Chinese Academy of Sciences, jointly unveiled the plaque for the institute. Gong Zheng noted that Shanghai, born by the sea and thriving by the sea, shoulders the major mission of serving the maritime power strategy. The establishment of the SJTU Institute of Deep-Sea Science and Engineering is conducive to the implementation of the maritime power strategy, the advancement of Shanghai's modern maritime city construction, and SJTU's progress towards becoming a world-class university. He expressed the hope that SJTU would construct the deep-sea major scientific facility to high standards and utilize it efficiently, playing a greater role in serving national strategies, exploring scientific frontiers, and developing the marine equipment industry. The Municipal Committee and Government will continue to support SJTU's development, jointly writing a new chapter of mutual achievement between a great city and a prestigious university. The "Far-Sea Floating Island" deep-sea major scientific facility is a national major science and technology infrastructure project and a world-first, super-large self-propelled scientific research platform for deep-sea operations. The Institute of Deep-Sea Science and Engineering, a directly-affiliated research platform of SJTU, will explore a new paradigm of organized research characterized by "constructing, researching, and producing output simultaneously," addressing the effective衔接 between...

2026年6月23日

2026年6月23日

Haizhongzhou actively integrates into the park's industrial chain, helping to build the ''blue engine''

As a key enterprise in Guannan Port Industrial Park, Jiangsu Haizhongzhou Shipping Industry Co., Ltd. actively integrates itself into the collaborative development pattern of the industrial chain, playing a leading role in the park's strategy of "strengthening, supplementing, and extending the chain." The Port Industrial Park serves as an important carrier for Guannan County's development of the marine economy. In recent years, the park has made every effort to develop the marine engineering equipment industry, gradually forming core industrial sectors such as steel smelting, green building materials, and shipbuilding and repair. The agglomeration effect of the port-oriented industrial system, characterized by export-orientation and large-scale operations, has begun to take shape. At the upstream of the industrial chain, the park has guided steel enterprises such as Yaxin Steel and Xingxin Steel to produce steel plates for shipbuilding, providing a stable supply of raw materials for our company and other shipbuilding enterprises. "This has significantly reduced our raw material procurement and transportation costs, enhancing our market competitiveness," said Lu Feng, Commercial Director of our company. The park is also accelerating the construction of a shipbuilding supporting industrial park, introducing manufacturers of marine motors and electronic components to further improve the shipbuilding industry system. At the midstream of the industrial chain, our company, together with three other shipbuilding enterprises, has fully implemented technological transformation and introduced new production processes. What used to be a "small shipyard" has now become a 100,000-ton-class shipbuilding base. Ship products have also shifted from traditional low-value-added deck barges to large bulk carriers, oil tankers, LNG hybrid-powered vessels, and other ship types. The chain-driven development has brought about a clustering effect. This year, the park's shipbuilding industry has witnessed a steady stream of good news. "As the only special shipbuilding industrial park in northern Jiangsu, the park will continue...

2026年6月23日

2026年6月23日

1,350 Ships! Container Ship Orders Surge to a Record High

Global Container Ship Orders Surge Against the Trend, Order Backlog Hits Record High. Chinese Shipbuilders Almost Monopolize the Recent Order Wave, Capturing Nearly 90% of New Orders This Year. Niels Rasmussen, Chief Shipping Analyst at the Baltic and International Maritime Council (BIMCO), stated that despite heightened uncertainty in trade policy and declining freight rates, the container ship order backlog continues to grow. The current total order book has exceeded 1,350 vessels, with a total capacity of 11.8 million TEU. In 2025, average global container ship freight rates fell by approximately 13% year-on-year. Meanwhile, increased import tariffs by the United States have sparked concerns over rising trade protectionism. Nevertheless, data shows that global container shipping volume still grew by 4.7% year-on-year last year, while new container ship orders reached a record 4.8 million TEU. Entering 2026, the container ship ordering boom continued in the first two months, with new orders reaching 102 vessels totaling 665,000 TEU. By the end of February, the container ship order book stood at 11.8 million TEU, a year-on-year increase of 28%. According to Rasmussen, very large vessels currently dominate the container ship order book, indicating a future trend in the global shipping network where large vessels will replace small and medium-sized ones. Currently, the order book for container ships of 12,000 TEU and above totals 436 vessels, accounting for 65% of the total order book in TEU terms. However, the fastest growth in the order book over the past year has actually been for small and medium-sized vessels. The order book for vessels under 3,000 TEU, between 3,000–6,000 TEU, and between 6,000–8,000 TEU has all doubled, while other vessel types saw an increase of only about 17%. BIMCO noted that the order book for these three categories of small and medium-sized container ships accounts for only...

2026年6月23日

2026年6月23日

Soaring oil prices, pressure on older vessels: dry bulk shipping is being repriced by high fuel costs

The impact of escalating tensions in the Middle East is no longer simply a matter of "rising oil prices." For the dry bulk shipping market, this round of shocks is rapidly transmitting to deeper operational logic: surging bunker fuel costs, increased difficulty in voyage quotation, charterers' preference shifting toward energy-efficient vessels, reassessment of the value of scrubber-fitted ships, renewed scrutiny of the geopolitical security of alternative fuels, and older, high-fuel-consumption vessels being pushed more quickly toward demolition. In its latest weekly report, BRS highlighted that the sharp rise in oil prices is fundamentally disrupting the existing fuel economy balance in the dry bulk sector. A geopolitical shock is rewriting the cost curve for dry bulk shipping BRS noted that following the outbreak of the Middle East conflict, global oil prices and bunker fuel prices have experienced sharp volatility amid concerns over a potential closure of the Strait of Hormuz. The Strait of Hormuz normally handles approximately 20 to 21 million barrels per day of crude oil and refined product shipments, making it one of the world's most critical energy shipping chokepoints. Against this backdrop, international oil prices rose rapidly, with ICE Brent front-month contracts trading above USD 100 per barrel at the time of writing. Price movements have become highly sensitive to news flow, with intraday volatility hitting record levels. This shift quickly transmitted to the bunker fuel market. BRS specifically noted that bunker fuel prices are highly correlated with crude oil prices, and fuel costs account for a significant proportion of voyage costs in the dry bulk sector. As a result, sharp fluctuations in fuel prices are eroding shipping companies' ability to provide stable quotations for new voyages. The report even mentioned that some operators have defaulted on contracts due to an inability to complete bunkering within agreed laycan...

2026年6月23日

2026年6月23日

Haizhongzhou Shipping Industry ltd is Busy and order in Production, Accelerating the Construction of Multiple Export Vessels.

Spring returns to the earth, and all things compete to flourish. Stepping into the factory area of Jiangsu Haizhongzhou Shipping Industry Co., Ltd., a bustling yet orderly production scene greets the eyes: welding sparks fly on the berths, gantry cranes rise and fall without cease, and workers are busy accelerating the construction of vessels for export orders, playing a stirring "prelude to spring." "Currently, the company's production tasks are full. Orders for this year are already fully booked, and orders for the first half of next year are also largely secured," introduced Deng Chi Huo, the relevant person in charge of Haizhongzhou Shipbuilding. Recently, the company has been accelerating the construction of multiple vessels for export to South Korea. Meanwhile, several container ship projects are under negotiation, maintaining the company's steady development momentum. In recent years, Haizhongzhou Shipbuilding has focused on its core businesses of shipbuilding, repair, demolition, and steel structure fabrication. It has continuously increased investment in technological upgrades, constantly optimizing key production factors such as berths and gantry cranes, steadily enhancing its shipbuilding and repair capabilities. The company has established long-term, stable cooperative relationships with numerous enterprises, with its undertaken vessel types covering fields such as bulk carriers, chemical tankers, electric propulsion ships, and tourism & leisure pontoons. Relying on good construction quality and delivery reputation, the company has successfully secured export orders for Indonesian container ships and offshore operating platforms, gradually establishing the "Haizhongzhou" brand image in the international market. Since the beginning of this year, the company's production and operation have maintained stable operation, laying a solid foundation for achieving the annual targets. Standing at a new starting point, Haizhongzhou Shipbuilding will continue to uphold the business philosophy of "Quality First, Integrity Based," seize opportunities in marine economy development, continuously enhance its core competitiveness, and contribute...

2026年6月23日

2026年6月23日

Order Backlog Exceeds KRW 200 Billion! Shipbuilding Giant Secures Additional Tanker Order

On March 10, South Korea's Samsung Heavy Industries (SHI) announced that it had signed a contract with a shipowner based in Bermuda for the construction of three crude oil carriers. These three new vessels are scheduled for delivery by the end of February 2029. The total contract value is KRW 400.1 billion (approximately USD 274 million, or CNY 1.878 billion), equivalent to a unit price of USD 91.27 million per vessel. SHI did not disclose the shipowner's identity, but JP Morgan has confirmed ordering three Suezmax crude oil carriers at SHI. For reference, data from Clarksons shows that the current newbuilding price for a 156,000-158,000 DWT Suezmax crude carrier is approximately USD 87.5 million, unchanged from the same period last year. This is JP Morgan's second order with SHI this year. Previously, in January, SHI secured an order from JP Morgan for two large LNG carriers, with a total contract value of approximately USD 500 million. These new vessels are scheduled for delivery by the end of January 2029. Including the latest order, SHI has won a total of 11 new vessel orders so far this year, valued at USD 2.1 billion (approximately CNY 14.5 billion), achieving about 15% of its annual order target of USD 13.9 billion. These 11 new vessel orders consist of 3 large LNG carriers, 2 Very Large Ethane Carriers (VLECs), 2 container ships, and 4 crude oil carriers. A representative from Samsung Heavy Industries stated, "Currently, the company's cumulative order backlog stands at 137 vessels, valued at USD 29.5 billion (approximately CNY 203.5 billion), securing a workload for over three years. Accordingly, in 2026, the company plans to continue its selective order-taking strategy, prioritizing profitability based on this stable backlog. In addition to LNG carriers, SHI is continuously expanding its order portfolio, focusing on high-value-added...

2026年6月23日

2026年6月23日

Crossing Thousands of Miles, Joining Hands for Blue Sea Win-Win——Kazakhstan Delegation Visits Jiangsu Haizhongzhou Shipping Industry Co., Ltd.

Recently, a delegation from the Republic of Kazakhstan paid a special visit to Jiangsu Haizhongzhou Shipping Industry Co., Ltd. for on-site inspection and business negotiations. As an important country in Central Asia, Kazakhstan has been making continuous efforts in the Caspian Sea shipping and inland waterway transportation sectors in recent years. This visit aimed to gain an in-depth understanding of our technical strength in shipbuilding and repair, and to explore new opportunities for bilateral cooperation. Accompanied by our senior management, the delegation delved into the front-line production areas, visiting the 10,000-tonne dock, CNC machining center, and outfitting quay in sequence. Witnessing large engineering vessels undergoing upgrading and modern tugs under sectional construction, the delegation members frequently paused to inquire, gaining detailed insights into the process flows, construction cycles, and technical parameters. Particularly regarding the application of green repair and construction technologies and special vessel modifications, our technical staff, using practical cases, vividly demonstrated Haizhongzhou's technological accumulation and innovative capabilities in complex projects. During the subsequent symposium, the company's leadership provided a comprehensive overview of our development history, overseas project achievements, and practical experience in participating in the "Belt and Road" construction. The head of the delegation stated that Jiangsu Haizhongzhou Shipbuilding Co., Ltd. demonstrated an impressive level of professionalism and production capacity. He noted that Kazakhstan has substantial demand in areas such as port construction along the Caspian Sea coast and the upgrade of river dredging equipment, indicating broad prospects for cooperation between the two sides. Subsequently, both parties engaged in pragmatic discussions focused on specific project requirements, technical standard alignment, and cooperation models, reaching preliminary consensus on further deepening collaboration. This inspection and exchange visit not only enhanced the Kazakhstan delegation's recognition of our comprehensive strength but also laid a solid foundation for substantive cooperation in the field of...

2026年6月23日

2026年6月23日

Chinese shipyards take the lead! The global shipping industry rides the wave of green transformation

Global shipping decarbonization is accelerating, with orders for alternative-fuel vessels remaining high in the first month of this year. Chinese shipyards have maintained a leading edge in this wave of green orders, becoming a key pillar in the global shipping energy transition. According to the latest statistics from Clarksons, of the 158 new vessels totaling 10.7 million gross tons (GT) ordered globally in January, as many as 46 vessels, accounting for 4.5 million GT, are alternative-fuel vessels. This represents 42% of the total, up from 37% for the full year of 2024. In terms of order value, global new shipbuilding investment in January totaled $17.8 billion, with the value of alternative-fuel vessel orders reaching $8.6 billion (approximately RMB 59.4 billion). This marks an 18% increase year-on-year and accounts for 48.1% of the total investment. January’s alternative-fuel vessel orders include 33 LNG-powered vessels totaling 4.0 million GT, one methanol-powered vessel of 0.1 million GT, five LPG-powered vessels totaling 0.3 million GT, two ethane-powered vessels totaling 0.1 million GT, and five battery/hybrid-powered vessels totaling 0.1 million GT. In recent years, the share of alternative-fuel vessels in new ship orders has climbed steadily, from just 8.2% in 2016 to 32% in 2021. It reached an all-time high of 54.9% in 2022, slipped to 41% in 2023, rebounded to 44% in 2024, and experienced a slight decline to 43.6% in 2025. By shipbuilding country, Clarksons' data shows that the vast majority of alternative-fuel new ship orders in January 2026 were secured by Chinese shipyards, totaling 36 vessels and 2.207 million compensated gross tons (CGT). By CGT, this accounts for 70.19% of all alternative-fuel vessel orders in January 2026, ranking first globally. These orders include 26 LNG dual-fuel vessels (1.932 million CGT), four LPG dual-fuel vessels (0.123 million CGT), three ethane dual-fuel vessels (92,000 CGT),...

2026年6月23日

2026年6月23日

The Seeds of Friendship Blossom Again – Indonesian Client Revisits Haizhongzhou, Continuing a New Chapter of Win-Win Cooperation

In February, the sea breeze in Lianyungang still carried a chill, yet the atmosphere inside Jiangsu Haizhongzhou Shipping Industry Co., Ltd. was filled with warmth and excitement. On February 10, a familiar face from afar once again appeared at the construction site of ten-thousand-ton vessels—a delegation of shipowners from Indonesia set foot on this land anew, embarking on their second in-depth visit to Haizhongzhou just months after their last trip. A Reunion that Witnesses Growth"Last year, what we saw was a busy construction site; this year, we are greeted by magnificent berths and giant vessels ready for launching," remarked the Indonesian client representative during the tour. From cautious observations during the first visit to the familiar and cordial exchanges now, this journey signifies not only the continuation of business cooperation but also the testament to a cross-border friendship. Accompanied by the company team, the Indonesian guests revisited the frontline production areas along the same route as last year. Compared to the scene twelve months ago, the 100,000-tonne berth now holds even more massive hull structures. The 300-tonne gantry crane operated efficiently while welding sparks danced like fireflies. The delegation carefully inspected the progress on the segmented construction of container vessels bound for Russia and spoke highly of the newly introduced intelligent production equipment. From Trust to RelianceFollowing the tour, both parties engaged in enthusiastic and candid discussions in the conference room. The Indonesian client expressed, "Haizhongzhou has not only fulfilled the promises regarding capacity upgrades made during our last visit but has also demonstrated impressive technological breakthroughs in specialized vessel construction. This time, we are not just visiting the shipyard—we are visiting our 'relatives'." The term "visiting relatives" perfectly captured the evolution of their relationship from mere business partners to strategic allies. Since last year, Haizhongzhou has built a strong...

2026年6月23日

2026年6月23日

As the wave of orders recedes, a tide of deliveries arrives! The car carrier market sounds the alarm

The four-year surge in orders for car carriers has drawn to a close, marking a turning point for the market. A large number of new vessels ordered during that period are now entering the delivery phase, ushering in a new wave of completions and raising concerns about potential overcapacity. According to a recent monthly report from AXSRoRo, a record 75 new car carriers were delivered in 2025, a significant jump from 12 in 2023 and 46 in 2024. Over the past three years, a total of 133 car carriers, with a combined capacity of approximately 990,000 CEU, have entered service. In 2026, deliveries are projected to reach 67 vessels (around 518,000 CEU), which would still be the third-highest annual total on record. Looking ahead, deliveries are expected to taper off to 50 vessels in 2027 and 26 in 2028. As this delivery wave gains momentum, the order boom that preceded it came to an end last year. Clarkson's data shows that only eight new car carrier orders were placed globally in 2024, the lowest number since just three were ordered in 2020. The recent ordering spree began in 2021, when orders surged to 39 vessels—more than the combined total of the previous five years—with a strong focus on large vessels of 6,000+ CEU. This trend continued through 2024, with annual orders reaching 75, 85, and 73 vessels in 2022, 2023, and 2024, respectively. AXSRoRo attributes the surge in orders primarily to the rapid growth of Chinese auto exports. In 2020, China's complete vehicle exports just exceeded 1 million units. By early 2021, monthly exports surpassed 100,000 for the first time. This figure climbed to 994,000 units by December 2025, a 21.4% increase month-on-month and a 73.2% increase year-on-year. This explosive growth propelled China past Japan, the long-time leader in global...

2026年6月23日

2026年6月23日

The demand for feeder container ships is experiencing a strong upward trend.

Driven by the structural transformation of global supply chains over the past year, the market demand for feeder containerships is experiencing significant growth. In its latest weekly report, shipbroker Intermodal noted that the global container shipping market had a relatively subdued start to 2026. As the Chinese Lunar New Year approaches on February 17, market activity has declined as expected. While the pre-holiday "rushed shipping" effect in December temporarily boosted demand, market momentum has now gradually cooled. Combined Impact of the "Chinese New Year Effect" and Geopolitical Dynamics Nikos Tagoulis, Senior Analyst at Intermodal, noted that the Chinese New Year effect is a significant seasonal factor suppressing short-term tonnage demand. Factories typically begin scaling down production two weeks before the holiday, leading to a decline in labor supply, with disruptions to supply chains often lasting three to five weeks. However, compared to short-term seasonal fluctuations, geopolitical dynamics play a more critical role in shaping long-term industry trends. Among these, the timeline for the restoration of navigation through the Suez Canal has emerged as the most significant source of market uncertainty. Currently, liner operators have adopted a divergent strategy: some are cautiously resuming Red Sea routes, while others continue to opt for detours via the Cape of Good Hope. Notably, a "hybrid approach" has emerged in the market, where low-value cargo is routed through the Suez Canal, while high-value cargo is diverted to safer alternative routes. Overall, avoiding the Red Sea remains the predominant choice. According to BIMCO data, Red Sea traffic volume in early January plummeted by 60% compared to three years ago. Despite signs of stabilization in the security situation, most shipowners are still adopting a "wait-and-see" approach due to the persistent threats posed by the Houthi forces. Tagoulis particularly highlighted a paradox facing the market: while resuming navigation...

2026年6月23日

2026年6月23日

Synergy for Shared Success, Navigating the Future Together — Haizhongzhou Holds 2026 Core Suppliers Conference

On February 5th, the 2024 Core Suppliers Conference of Jiangsu Haizhongzhou Shipping Industry Co., Ltd., themed "Synergy for Mutual Success, Sailing Together Toward the Future," was grandly held at the company. More than 60 representatives from core equipment, material, and service suppliers across the country gathered to discuss cooperation and explore shared development. The conference reviewed the cooperative achievements of the past year and recognized outstanding suppliers for their exceptional performance in quality, delivery, and service. Representatives from the company’s procurement and production departments provided detailed updates on the current shipbuilding market landscape, the company’s future product plans, and production schedule requirements. This enabled supplier partners to gain a clearer understanding of demand trends and prepare resources in advance. In the face of increasingly fierce market competition and higher client demands for vessel quality and delivery cycles, Haizhongzhou Shipbuilding emphasized the critical importance of building a more stable, efficient, and trustworthy supply chain system. The company proposed its commitment to establishing deeper relationships with core suppliers, shifting from mere "business cooperation" to "strategic collaboration." This will involve closer cooperation in areas such as early-stage alignment on technical standards, joint quality process control, collaborative exploration of cost optimization, and coordinated mitigation of fulfillment risks. "Shipbuilding is a complex systematic project, and the successful delivery of every vessel relies on the strong support of our supply chain partners," said Deng Cihuo, Vice General Manager of the company, in his concluding remarks. "We hope to forge an even closer community of shared destiny with our partners. Through information sharing and capability co-building, we aim to jointly enhance the resilience and competitiveness of the industrial chain, navigating steadily through market challenges hand in hand."

2026年6月23日

2026年6月23日

Freight Rates Continue to Decline! SCFI Index Falls for Four Consecutive Weeks.

The pre-Chinese New Year shipment rush is winding down, with the Shanghai Containerized Freight Index (SCFI) declining for the fourth consecutive week and the pace of decline accelerating further. According to the latest data released by the Shanghai Shipping Exchange on January 30, the SCFI index dropped by 141.11 points last week to 1,316.75 points, representing a weekly decline of 9.67%. All four major long-haul shipping routes recorded declines, with each falling by more than 10%. On the Far East to West Coast North America route, freight rates per FEU fell by $217 to $1,867, a weekly decline of 10.41%. On the Far East to East Coast North America route, rates per FEU dropped by $291 to $2,605, a weekly decrease of 10.04%. On the Far East to Europe route, rates per TEU decreased by $177 to $1,418, a weekly decline of 11.09%. On the Far East to Mediterranean route, rates per TEU fell by $332 to $2,424, a weekly drop of 12.05%. On the regional routes, freight rates per TEU from the Far East to Kansai, Japan, remained unchanged from the previous week at $312, while rates to Kanto, Japan, also held steady at $321. Rates to Southeast Asia fell by $13 to $483 per TEU, and rates to South Korea remained unchanged at $144. Industry insiders note that the current spot market freight rates for container shipping companies are approximately $1,650 to $1,750 per FEU for the West Coast North America route, $2,350 to $2,500 for the East Coast North America route, and $2,000 to $2,200 for the Europe route. Several shipping companies have announced that the current rates will remain in effect until the end of February, indicating that rate adjustments may not occur until early March. Shipping companies explain that the extended Chinese New Year holidays...

2026年6月23日

2026年6月23日

New routes are proliferating! Shipping giants are "fleeing" the main lanes.

Global Shipping Shifts from "Trunk-Route Reliance" to "Multi-Polar Dispersion": New routes to Africa, the Middle East, and Southeast Asia are witnessing concentrated maiden voyages, driven by both organic demand and strategic responses to uncertainty. According to ALPHALINER data, as of the end of November 2025, the Trans-Pacific route, which carries the core of global east-west trunk trade, is under pressure, with capacity contracting by 2.9% year-on-year. Meanwhile, in early Spring 2026, a wave of maiden voyages on new routes to regions like the Middle East and Southeast Asia, combined with capacity restructuring on traditional lanes and port infrastructure upgrades, is accelerating the evolution of global trade from a "traditional trunk-route dependence" towards a decentralized, "multi-polar" pattern. This transformation is driven by both organic market forces and the shipping industry's strategic adaptation to an uncertain environment. The China Shipping Prosperity Report, released by the Shanghai International Shipping Institute on January 6, 2026, indicates that although China's Shipping Prosperity Index remained in the relatively prosperous zone at 112.23 points in Q4 2025, it is forecast to drop to 106.69 points (marginally prosperous zone) in Q1 2026. The confidence index is expected to fall even more sharply from 120.20 points to 96.12 points (slightly below the prosperity threshold), highlighting the industry's apprehension about future market volatility. Emerging Markets: New Routes Forming a Denser "Capillary" Network Within less than a month of 2026's start, several landmark maiden voyages have been launched in Southeast Asia, Africa, and the Middle East. These routes, characterized by "high efficiency, green practices, and customization," not only fill gaps in regional trade corridors but also reshape the logistics competitiveness of emerging markets through technological upgrades and network synergy. In Southeast Asia, a revolution in express shipping with 7-day direct services and "land-sea coordination" is underway. On January 5th, the departure of the vessel Tongdan from Shanghai's Waigaoqiao Phase V...

2026年6月23日

2026年6月23日

Deepening Cooperation, Charting a Shared Future--Indonesian Partners Revisit Jiangsu Haizhongzhou Shipbuilding for Inspection and Exchange

Following their successful visit in December last year, representatives from a well-known Indonesian shipping company recently revisited Jiangsu Haizhongzhou Shipping Industry Co., Ltd. for an in-depth inspection and technical discussions on specific collaborative projects. Mr. Deng Cihuo, Deputy General Manager of the company, along with the technical team, warmly received the old friends from afar. Both sides engaged in fruitful exchanges in a friendly and pragmatic atmosphere. During this visit, the delegation focused on touring the company’s newly built intelligent production workshop and digital design center. They observed the entire construction process of container bulk carriers tailored for Southeast Asian clients. In the technical exchange session, the company’s engineers detailed the technological improvements designed for tropical sea navigation, including enhanced anti-corrosion coating systems, high-efficiency air conditioning and ventilation systems, and navigation equipment configurations adapted to multi-reef sailing environments. The Indonesian clients paid particular attention to the vessels’ fuel efficiency and maintenance convenience. In response, the technical team presented the latest hull optimization data and modular equipment design solutions. During the symposium, both parties reviewed the progress made since last year’s visit and engaged in substantive discussions on details such as technical specifications of specific ship models, construction timelines, and after-sales service guarantees. The Indonesian representatives expressed confidence in Haizhongzhou Shipbuilding’s technical capabilities and quality management system after multiple on-site inspections and looked forward to advancing the collaboration to a new stage. This revisit marks the transition of the cooperation into a substantive implementation phase, demonstrating the continued recognition of the company’s professional expertise by international clients. Jiangsu Haizhongzhou Shipping Industry Co., Ltd. will continue to uphold technological innovation and refined management, delivering high-quality products and services to repay the trust of its clients. The company remains committed to contributing to the implementation of the Chinese shipbuilding industry’s "going global" strategy...

2026年6月23日

2026年6月23日

Tanker Market Watch: Following Venezuela, Iran Continues to Stir the Market

With the situation in Venezuela temporarily subsiding, the focus of the tanker market has shifted back to Iran. In its latest weekly report, shipbroker Gibson pointed out that, at present, the Iranian authorities appear to have quelled most of the unrest. However, the threat of potential attacks by the United States, disruptions in Black Sea exports, and the ongoing developments in Venezuela continue to keep the oil and shipping markets on edge. Predictions regarding the direction of potential incidents—such as U.S. attacks, escalated protests, or regime change—remain highly uncertain. Gibson’s analysis suggests that attacks targeting Iran in the short term pose the greatest risk. The Islamic Revolutionary Guard Corps has warned that any aggression would trigger large-scale retaliation across the region. The primary threats still lie in potential disruptions to shipping through the Strait of Hormuz and attacks on oil facilities in the area. Should conflict break out, the Houthi forces could also resume their assaults on vessels. Under such circumstances, insurance premiums and freight rates would inevitably rise, reflecting an increase in regional risk premiums. Furthermore, the potential impact of regime change on oil production cannot be overlooked. Despite increasing sanctions pressure, Iran remains a major oil supplier. According to FGE data, the country's total oil production increased to 5.18 million barrels per day last year (including 3.64 million b/d of crude oil, 800,000 b/d of condensate, and 730,000 b/d of natural gas liquids), reaching a new high since the 1970s. Conversely, if a reconciliation is reached with Washington, it could normalize Iran's oil exports. Although this process may take years, its impact on the tanker market would be profound. During the peak period of sanctions relief in 2017, Iran exported over 2.5 million barrels of crude oil to international markets, while last year's exports are estimated at 1.5...

2026年6月23日

2026年6月23日

186 Vessels!The order volume of Japan shipyard has declined for four consecutive years

Japanese Shipbuilders' 2025 Order Volume Declines 20% Year-on-Year, Marking Fourth Consecutive Year of Downturn Recently, the Japan Ship Exporters' Association (JSEA) released the full-year order data for Japanese shipbuilders in 2025. Last year, Japanese shipbuilders secured orders for a total of 186 vessels, amounting to 8,936,514 gross tons (GT), representing a decrease of 19.9% compared to 2024's 251 vessels (11,160,206 GT). The number of vessels ordered fell by 65. By vessel type, the new ship orders received by Japanese shipbuilders last year included 147 bulk carriers totaling 6,510,390 GT, a reduction of 49 vessels year-on-year. Among these, Handysize bulk carriers increased by 2 vessels to 59, making them the only segment to achieve growth. Ore carriers remained steady at 2 vessels, unchanged from 2024. Capesize bulk carriers decreased by 3 vessels to 25, showing a relatively minor decline. In contrast, Supramax bulk carriers fell by 16 vessels to 53, Panamax bulk carriers dropped by 20 vessels to 5, and Post-Panamax bulk carriers decreased by 11 vessels to 3. While there was one cement carrier order in 2024, no such orders were recorded in 2025. Last year, Japanese shipbuilders received a total of 25 cargo vessel orders (1,492,474 GT), an increase of 1 vessel year-on-year. Among these, container ships rose by 9 vessels to 18, and car carriers increased by 1 vessel to 2, while general cargo vessels decreased by 9 vessels to 5. Tanker orders amounted to 13 vessels (933,170 GT), a reduction of 18 vessels year-on-year. Among these, VLCCs increased by 2 vessels to 4, and Aframax tankers rose by 1 vessel to 2. However, LPG carriers decreased by 5 vessels to 1, LPG/liquid ammonia carriers fell by 4 vessels to 2, and chemical tankers dropped by 7 vessels to 4. Orders for Suezmax tankers (3 vessels in 2024),...

2026年6月23日

2026年6月23日

Gathering Strength through Talent Cultivation: Jiangsu Haizhongzhou Shipbuilding Launches Inaugural "Artisan Star" Class

To solidify the foundation for the company's development and forge a first-class industrial workforce, Jiangsu Haizhongzhou Shipping Industry Co., Ltd. recently officially launched its inaugural "Artisan Star Program" high-skilled talent training class. Over fifty outstanding young welders, assemblers, and pipe fitters from the production frontlines became the first batch of trainees, embarking on a systematic journey of skills enhancement. Shipbuilding is a technology-intensive industry, where craftsmanship spirit and masterful skills are fundamental to ensuring the "seaworthy" quality of every vessel. The company deeply recognizes that a highly skilled industrial workforce is at the core of its competitiveness. This "Artisan Star" class is a crucial component of the company's systematic talent strategy, designed to rapidly cultivate a group of on-site technical leaders who understand processes, excel in operations, and are adept at innovation through a comprehensive training model of "theoretical in-depth study and training, hands-on tempering, and mentorship by experts." The training curriculum is closely aligned with the demands of modern shipbuilding processes, covering core content such as advanced welding techniques, digital blueprint interpretation, precision control standards, application of advanced tooling, and safety production protocols. The company specially invited a panel of lecturers comprising internal senior technicians, senior engineers, and external industry experts to ensure the foresight and practicality of the training. Vice General Manager Deng Cihuo emphasized at the opening mobilization meeting: "We must not only build excellent ships but also cultivate excellent people. The 'Artisan Star Program' is a long-term platform. We hope all trainees cherish this opportunity, immerse themselves in research, translate what they learn into practical actions that pursue exquisite craftsmanship, strive to become the backbone of the company's transformation and upgrading, and contribute their artisan wisdom to forging the 'Haizhongzhou' golden brand." This initiative not only helps enhance the company's overall manufacturing standards but also provides employees...

2026年6月23日

2026年6月23日

Overcapacity! SCFI Index Falls for Two Consecutive Weeks.

The fundamental oversupply in the container shipping market remains unchanged, and the Shanghai Containerized Freight Index (SCFI) continued to decline last week. According to the latest data released by the Shanghai Shipping Exchange on January 16, the SCFI dropped by 73.27 points last week to 1,574.12 points, with the weekly decline widening to 4.45%. Among the four major long-haul routes, freight rates for three declined, with only the U.S. East Coast route experiencing a slight increase. Last week, freight rates from the Far East to the U.S. West Coast fell by $24 per FEU to $2,194, a weekly decline of 1.08%. Rates from the Far East to the U.S. East Coast rose by $37 per FEU to $3,165, a weekly increase of 1.18%. Freight rates from the Far East to Europe dropped by $43 per TEU to $1,676, a weekly decrease of 2.5%. Rates from the Far East to the Mediterranean fell sharply by $249 per TEU to $2,983, a weekly decline of 7.7%. On regional routes, freight rates from the Far East to Japan’s Kansai region remained unchanged at $312 per TEU, as did rates to Japan’s Kanto region at $321 per TEU. Rates to Southeast Asia declined by $9 per TEU to $515, while rates to South Korea rose by $2 per TEU to $144. Industry insiders noted that the growth rate of container ship capacity continues to outpace the increase in actual cargo volumes, with short-term freight rates still significantly impacted by overall capacity supply. Despite some pre-Chinese New Year shipment demand, it remains difficult to fully absorb supply in the short term. As the market supply and demand have not yet fully rebalanced, the short-term market is expected to remain volatile. Between January 15 and 21, alliance route rates remained relatively stable, with U.S. West Coast...

2026年6月23日

2026年6月23日

Subsidy Rules for Scrapping and Renewal of Old Operating Vessels Released, Policy Effective Until 2028!

Recently, the Ministry of Transport and the National Development and Reform Commission jointly issued the "Implementation Rules for Subsidies on the Scrapping and Renewal of Old Operating Vessels (Revised Version)" (referred to as the "Implementation Rules"). This document further clarifies the scope and standards of subsidies, the application and review process for subsidies, as well as the requirements for managing subsidy funds. The aim is to drive a new round of fleet renewal for old operating vessels and adjust the structure of ship capacity. According to the "Implementation Rules," the subsidy policy is effective from August 2, 2024, until December 31, 2028. Shipowners may apply for subsidy funds for eligible old operating vessels that are scrapped and for newly built fuel-powered vessels (including those using biodiesel) or new energy/clean energy vessels. The scrapping and renewal of old operating vessels will adopt differentiated subsidy standards based on vessel type, vessel age, and the propulsion type of the newly built vessel. These standards will be dynamically adjusted according to the shipping market conditions. The subsidy standard for newly built dual-fuel coastal vessels follows that of fuel-powered vessels. The subsidy amount for a newly built inland vessel shall not exceed 40 million yuan. New energy/clean energy vessels that receive subsidies must not alter their propulsion form or undergo modifications that reduce their fuel substitution rate for 10 years after construction is completed. The "Implementation Rules" specify that applications for subsidies for the scrapping and renewal of old operating vessels should be submitted, along with relevant supporting documents, to the municipal transport authorities at the prefecture level where the vessel's port of registry is located. Effective from the release date of these rules, for applications seeking subsidies for newly built new energy/clean energy vessels, the "Ship Survey Certificate" must be issued after the China...

2026年6月23日

2026年6月23日

Warmly Celebrate the Smooth Launching of the Newly Built Vessel "Xin Boyuan" by Jiangsu Haizhongzhou Shipping Industry Co., Ltd.

Recently, at the shipbuilding base of Jiangsu Haizhongzhou Shipping Industry Co., Ltd. , colorful flags fluttered and fireworks lit up the sky, filling the air with a jubilant and lively atmosphere. A new modern vessel meticulously built by our company for a renowned domestic shipowner—the "Xin Boyuan"—successfully slid off the construction berth and made a perfect launch at an auspicious morning hour on January 13, 2026, amid the watchful eyes and blessings of all in attendance. The "Xin Boyuan" is another masterpiece crafted by Haizhongzhou in adherence to the philosophy of "pursuing excellence and prioritizing customers." The vessel features advanced design, high technological sophistication, and superior overall performance. During its construction, a significant number of new energy-saving and environmentally friendly technologies and equipment were incorporated. It meets advanced domestic standards in terms of fuel economy, navigation safety, and emission environmental benchmarks, fully reflecting the industry trend toward green and intelligent shipbuilding. Since the commencement of the "Xin Boyuan" construction, the company has placed great emphasis on the project. The project team worked closely with the shipowner and ship inspection parties, overcoming multiple challenges such as tight construction schedules and complex technical processes. All personnel involved demonstrated the traditional Haizhongzhou spirit of unity, dedication, and tackling difficulties head-on. They strictly followed production procedures, prioritized quality management and safety, ensuring the high-quality and efficient completion of tasks at each construction milestone. This successful launch marks a crucial priod victory in the construction of the "Xin Boyuan," laying a solid foundation for subsequent outfitting, debugging, and sea trials. During the simple yet solemn launching ceremony, the shipowner's representative highly commended our company's construction quality, management standards, and team collaboration. They also expressed firm confidence in the future continuous cooperation between both parties. In his address, the company's leadership extended heartfelt gratitude to all...

2026年6月23日

2026年6月23日

Chinese shipbuilding industry still"the absolute protagonist"!The global holding order has hit it's record

Although global new ship orders have retreated from their peak, the shipbuilding industry in 2025 did not fall into a downturn. On the contrary, supported by a record-high order backlog over the past 16 years and the accelerated restart of global shipbuilding capacity, the industry as a whole maintained a relatively high level of activity. As the "absolute protagonist" in the global shipbuilding market, China's shipbuilding industry continues to lead the world in three key indicators, further consolidating its dominant position. According to data from Clarksons, global new ship orders in 2025 totaled 2,036 vessels, representing 151 million deadweight tons (dwt) and 56.42 million compensated gross tons (CGT). In terms of dwt, this marked a 24% decline compared to the 199 million dwt in 2024 (the highest level since 2007). The total value of new ship orders was approximately $181.3 billion (about ¥12.6 trillion RMB), which, although lower than the $230 billion in 2024, remains the second-highest annual record since 2008 ($184.1 billion). Clarksons’ recent 2025 Shipbuilding Industry Review noted that, in terms of vessel types, the dominant force in the newbuilding market last year remained container ships, accounting for 41% of all orders. Throughout 2025, new container ship orders reached 644 vessels with a capacity of 4.76 million TEU, surpassing the 2024 figure of 4.67 million TEU to set a new historical record. The total value of these orders amounted to approximately $59.4 billion (about ¥4.14455 trillion RMB). Among these, 73% of new container ship orders were placed by container shipping companies. Despite uncertainty surrounding emission regulations, 65% of new container ship orders in terms of TEU were for alternative-fuel vessels last year. In contrast, other vessel types saw varying degrees of decline in new orders. In the tanker segment, although the year ended strongly, annual new orders fell by 31% year-on-year, dropping from 61.1 million dwt in 2024 to 42.4 million dwt in 2025. Bulk carrier new orders...

2026年6月23日

2026年6月23日

Two Chinese Shipyards Split the Order! Global Commodity Giant Continues to Increase Investment with New Major Contract

Global commodity trading giant Mercuria Energy Group has once again moved to expand its fleet by placing new shipbuilding orders with two Chinese shipyards. According to reports, Mercuria recently placed orders for 2+2 Newcastlemax bulk carriers of 211,000 deadweight tons and two LR2 product tankers of 115,000 deadweight tons. The bulk carrier order was secured by Nantong Xiangyu Shipbuilding, while the tanker order was awarded to Dalian Shipbuilding Industry Co., Ltd. (DSIC). All new vessels will be powered by conventional fuels. The 2+2 bulk carriers ordered by Xiangyu Shipbuilding are priced at approximately $77.5 million per vessel. If the optional orders are confirmed, the total contract value will reach about $310 million (equivalent to RMB 2.165 billion). The two confirmed vessels are scheduled for delivery in 2028. For reference, Clarksons data shows that the current newbuilding price for a 210,000–212,000 deadweight ton Newcastlemax bulk carrier is $78 million (equivalent to RMB 544 million), slightly lower than the $79 million recorded in the same period last year. Meanwhile, the tanker order awarded to DSIC is priced at approximately $72 million per vessel, bringing the total value for the two ships to about $144 million (equivalent to RMB 1.005 billion). These vessels will be constructed by DSIC's subsidiary, Shanhaiguan Shipbuilding Industry, with deliveries expected in 2028 and 2029. Clarksons data indicates that the current newbuilding price for a 113,000–115,000 deadweight ton LR2 product tanker is approximately $75 million (equivalent to RMB 523 million), down about 4% from the $78 million recorded in the same period last year. Industry insiders note that Mercuria's bulk carrier order is part of the company's fleet renewal and expansion plan, marking its first acquisition of Newcastlemax bulk carriers for its owned fleet. Mercuria first entered the dry bulk shipping segment in early 2023 and currently owns two...

2026年6月23日

2026年6月23日

Haizhongzhou Establishes Special Task Force to Systematically Advance Welding Quality Improvement

To systematically enhance the quality of core shipbuilding processes, Jiangsu Haizhouzhong Shipping Industry Co., Ltd. officially established the "Welding Quality Special Improvement Team" at the end of 2025. The team is led by the company's Quality Department and brings together technical experts from the block assembly and section workshops under the Production Department. Additionally, it includes on-site surveyors from the China Classification Society (CCS) as technical advisors, forming a collaborative "internal execution + external supervision" operational mechanism. The team’s primary task is to standardize the processes for high-frequency welds in production. In the initial phase, the team focused on six common weld types, including fillet welds, vertical butt welds, and horizontal welds. Based on the latest national standards and classification society requirements, a comprehensive review and detailed revision of the existing process specifications were conducted. Key revisions included clarifying welding parameter ranges for different plate thickness combinations, standardizing pre-weld cleaning and preheating requirements, and unifying inspection criteria for weld appearance and internal quality. Based on these revisions, the team compiled illustrated versions of the New Edition Welding Operation Instruction Manual and the Typical Defect Identification and Repair Guide. The new process documents were first piloted in the hull section workshop and some outfitting manufacturing areas. During the pilot phase, the team implemented a "process card" system, where welders worked daily using cards that clearly specified the weld joint type, applicable parameters, and key control points for their shift. Meanwhile, the frequency of quality inspections was increased, and rapid weld dimension measurement tools were introduced, enabling real-time recording and analysis of process data. After nearly three months of pilot operation, the effectiveness of the specialized management was reflected in key data: the first-pass qualification rate for welding in the two pilot areas during classification society inspections steadily increased from an average of 92% before...

2026年6月23日

2026年6月23日

The world's most powerful "power bank" freighter—the "Ningyuan Diankun"—is rewriting a century of maritime fuel history with zero engine roar.

A ten-thousand-ton giant capable of carrying 742 containers yet sailing almost silently—this is not science fiction but the already launched “Ningyuan Diankun.” Its secret lies in an “electric heart” equivalent to that of 300 electric cars. With a length of 127.8 meters and a width of 21.6 meters, it is the world’s largest all-electric container ship. What truly sets it apart, however, is its engine room: instead of massive diesel generators, it is powered by ten standardized box-type batteries. With a total capacity of about 19,000 kWh—equivalent to the combined battery capacity of over 300 household electric vehicles—they form its robust “electric heart.” This heart enables the ship to sail approximately 90 nautical miles on a single charge, saving about 580 tons of fuel annually and reducing CO₂ emissions by over 1,400 tons. In port, it can be rapidly charged via high-voltage systems or undergo entire battery swaps via crane—much like replacing a phone battery. Solar panels on the deck also convert sunlight into electricity, making every “breath” it takes green. More than just an electric ship, it is an intelligent vessel that “thinks.” Equipped with a smart navigation system, it can autonomously plan routes, avoid collisions in real time, and even be controlled remotely. The launch of the “Ningyuan Diankun” marks the official entry of coastal shipping into a new era of all-electric propulsion and intelligent control. The gentle ripples it leaves as it slips into the water may seem soft, yet they are powerful enough to propel the entire shipping industry toward a cleaner, more sustainable future.

2026年6月23日

2026年6月23日

Chinese Shipyards "Dominate"! Container Ship Orders Hit Another Record High!

In the year 2025 that just ended, the global new shipbuilding market experienced an overall cooling, yet new orders for container ships once again set a historical record. Chinese shipyards continued to expand their advantage, securing over 70% of global orders and becoming the absolute leader in the field of container ship construction. According to data from Clarksons, global new ship orders in 2025 decreased by 27% compared to the high level in 2024 but still exceeded the average order volume from 2021-2023. Container ships remained the most prominent sector, with annual new orders reaching a record high of 644 vessels (4.759 million TEU), surpassing the previous record of 4.674 million TEU set in 2024. The total investment in new container ship construction in 2025 also further increased to $59.364 billion (approximately RMB 4.15183 trillion), slightly higher than the $58.568 billion in 2024. Chinese shipyards continued to lead the global container ship construction market, with particularly outstanding performance. Statistics from Clarksons as of December 30, 2025, show that nearly all new container ship orders in 2025 were secured by Chinese and South Korean shipyards. Among these, Chinese shipyards signed new orders for 518 vessels (approximately 3.446 million TEU), accounting for a market share of 72%. Meanwhile, South Korean shipyards secured new orders for 105 vessels (1.247 million TEU), representing a market share of about 26%. Among the hold order top 10 single shipyard,it has 7 shipyard from China.And Zhoushan Changhong international secured orders for 46 vessels with a total capacity of 523,000 TEU ,which has markedly surpass the Korean HD (49 vessel with a total capacity of 503,000 TEU) ,ranked first globally .The Korean Hnhua ocean ranked in third,it's order for 17 vessel with a total capacity of 307,000TEU;The Hengli Heavy industry and the Guangchuan International ranked in forth and fifth seperately,the order are...

2026年6月23日

2026年6月23日

415 Ships! New Order Volume Plummets! Is the Green Shipping Market Heading into "Winter"?

In 2025, the overall prosperity of the global newbuilding market has declined, and the growth rate of alternative-fuel vessel orders has also slowed down from its previous high level. Against the backdrop of multiple factors—including unestablished fuel technology pathways, increasing cost pressures, and uncertain regulatory expectations—shipowners' investment attitude toward green vessels has become markedly more cautious. According to the latest statistics from Clarksons, from January to November this year, out of a total of 1,627 new ship orders worldwide (87.6 million gross tons), as many as 415 vessels (35.9 million gross tons) are alternative-fuel ships, accounting for 41% of the total—lower than the 45% recorded for the entire previous year. In terms of order value, the global newbuilding investment from January to November this year totaled $146.7 billion, with the value of alternative-fuel ship orders amounting to $69.2 billion (approximately RMB 484.8 billion), a year-on-year decrease of 34%. This accounted for 47.2% of the total investment. The alternative-fuel vessel orders this year include 217 LNG-powered ships (28.7 million gross tons), 51 methanol-powered ships (5.2 million gross tons), 17 LPG-powered ships (0.7 million gross tons), 4 ethane-powered ships (0.1 million gross tons), and 132 battery/hybrid propulsion ships (1.7 million gross tons). In recent years, the proportion of alternative-fuel vessels in new ship orders has been steadily rising, increasing from just 8.2% in 2016 to 32% in 2021, and reaching an all-time high of 54.8% in 2022. After dropping to 41% in 2023, it rebounded to 45% in 2024. In terms of shipbuilding nations, Clarksons' data shows that in November 2025, the majority of new alternative-fuel vessel orders were taken by South Korean shipyards, with a total of 23 vessels (1.31 million CGT). By CGT, this accounted for 53.52% of the global alternative-fuel new orders in November 2025, ranking first worldwide. All...

2026年6月23日

2026年6月23日

Counting down the 10 most distinctive ships built by Chinese shipyards in 2025.

In 2025, China's shipbuilding industry once again demonstrated its strength on the global stage, delivering an impressive annual performance. As in previous years, the International Shipping Network has selected the 10 most distinctive new ships (note: ranked by delivery date) from among the numerous vessels delivered by Chinese shipyards throughout the year. This comprehensive review highlights the outstanding achievements of China's shipbuilding sector over the past year and looks forward to Chinese shipbuilders continuing to scale new heights on the path of high-quality development in 2026. 1.The world's most powerful pile driving ship, "Erhang Changqing" On January 5th, the delivery ceremony for the 150-meter pile-driving vessel "Erhang Changqing," built by Zhenhua Heavy Industries for China Communications Second Harbor Engineering Bureau, was held at Zhenhua Heavy Industries. This vessel boasts the world's tallest pile frame, the largest pile-lifting capacity, the longest driving capability, and the strongest resistance to wind and waves. With an overall length of 130.5 meters, a molded breadth of 40.8 meters, a molded depth of 8.4 meters, and a pile frame height of 150 meters, the vessel is capable of driving piles with a maximum weight of 700 tons and a diameter of 7 meters. The vessel is the first in the industry to adopt a diesel-electric hybrid DC grid system equipped with supercapacitors, significantly improving fuel efficiency and reducing carbon emissions. It features the world's largest 5,000-ton thrust ultra-large hydraulic cylinder, independently developed and manufactured in China. Additionally, it is equipped with a pile-driving positioning system with offshore satellite differential capabilities, enabling centimeter-level precision in deep-sea pile-driving operations. The vessel also incorporates an intelligent pile-driving operation management system that integrates real-time hydrological parameter sensing, operational decision support, automatic process identification, and automated pile-driving data generation. This system effectively enhances the intelligence and digitalization of vessel operations, setting...

2026年6月23日

2026年6月23日

Oceans Embrace All Rivers, Together We Build the Voyage—Jiangsu Haizhongzhou Shipping Industry Co., Ltd. Warmly Welcomes Distinguished Mexican Clients for an Inspection Visit.

On December 29, Jiangsu Haizhongzhou Shipping Industry Co., Ltd. welcomed esteemed guests from afar—key representatives from a major Mexican shipping enterprise. Led by Mr. Lu Feng, the Commercial Director, the company’s management and technical team greeted the visitors with full enthusiasm and professionalism at their modern shipbuilding base located along the Yangtze River. A comprehensive and productive inspection and exchange event was organized for the guests. This visit aimed to deepen mutual trust, showcase the comprehensive capabilities and technical expertise of Haizhongzhou Shipping Industry, and facilitate in-depth discussions on potential collaborative projects. Upon arrival, the delegation first attended a detailed presentation in the company’s exhibition hall, covering Haizhongzhou’s development history, core business areas, technical strengths, and notable achievements. Exquisite ship models, detailed data, and vivid project cases clearly outlined the company’s end-to-end service capabilities—from design and construction to delivery—as well as its extensive experience in key vessel types such as bulk carriers and multi-purpose vessels. Subsequently, accompanied by Director Lu and technical staff, the Mexican clients conducted an on-site inspection of the production facilities. The tour covered the entire core process of shipbuilding—from the well-organized steel pretreatment and cutting center to the advanced and efficient planar block assembly line; from the towering dock and the large vessels being assembled under the gantry cranes to the precision machining of components in the workshops, and finally to the nearly completed new ships ready for sea trials at the pier. Throughout the tour, the company’s representatives provided detailed explanations and live demonstrations on key topics of interest to the clients, including production processes, quality control systems, environmental standards (such as EEDI and ballast water treatment), and construction cycle management. The tidy workshop environment, standardized operational procedures, the focused demeanor of the workers, and the highly automated production equipment left a deep impression on...

2026年6月23日

2026年6月23日

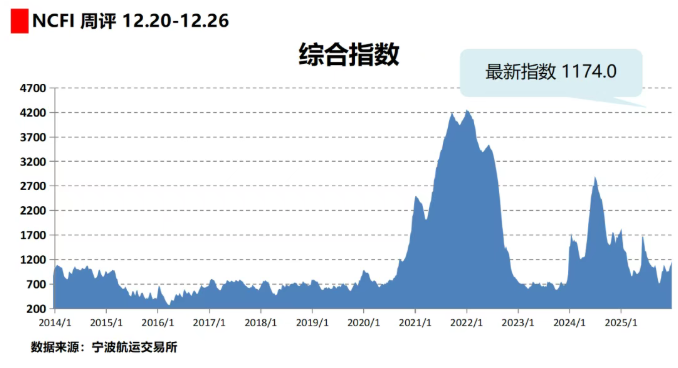

Maritime Silk Road Index: Overall Demand Continues to Rise, Freight Rates Increase on Most Routes.

This week, the Ningbo Containerized Freight Index (NCFI), part of the Maritime Silk Road Index released by the Ningbo Shipping Exchange, closed at 1174.0 points, up 7.2% from last week. Among the 21 shipping routes, freight rate indices increased on 17 routes, decreased on 3 routes, and remained largely flat on 1 route. Among the major ports along the Maritime Silk Road, freight rate indices rose at 9 ports, fell at 6 ports, and remained largely unchanged at 1 port. Key route index developments for this reporting period are as follows: Europe & Mediterranean Routes: Market cargo volume was relatively high, with shipping lines announcing freight rate increases for early January 2026. Rising shipment activity further tightened space availability, leading to higher freight rates. The Europe route index stood at 1144.4 points, up 7.2% from last week. The East Mediterranean route index was 1650.9 points, up 19.0% from last week. The West Mediterranean route index was 2053.9 points, up 16.5% from last week. North America Routes: Overall transport demand was limited, but shipping lines reduced route capacity, leading to stable or slightly rising freight rates. The East America route index was 1065.7 points, up 2.3% from last week. The West America route index was 1254.9 points, up 2.2% from last week. Middle East Routes: Freight rates remained at relatively high levels in the previous period, but insufficient growth momentum on the demand side led to only a slight increase in rates. The Middle East route index was 1505.8 points, up 1.0% from last week. South Africa Routes: Significant volatility was observed this week. After multiple rounds of reductions, freight rates had fallen to low levels earlier. Market shipments improved, and shipping lines imposed peak season surcharges, resulting in a substantial rise in freight rates. The South Africa route index was...

2026年6月23日

2026年6月23日

Haizhongzhou Shipping industry,CO,LTD Distributes New Year's Day Holiday Benefits to All Employees

With the approach of the New Year's Day holiday, to express gratitude for the hard work of all employees throughout the year, Jiangsu Haizhongzhou Shipping Industry Co., Ltd. distributed holiday benefits to all staff members on December 26, adding a warm festive atmosphere to the upcoming New Year. The New Year's Day benefits were designed with practicality and thoughtfulness in mind, primarily consisting of two parts: a traditional holiday food gift set, including selected grain and oil, nuts, and local specialty agricultural products; and a daily necessities kit, containing items such as insulated cups and towels. The benefits were distributed in an orderly manner by each workshop and department on the morning of December 26. At the distribution site, employees collected their benefits in an orderly manner, creating a harmonious atmosphere. A senior worker from the hull workshop remarked, "The items are practical and useful for daily life. It’s heartwarming that the company remembers us every year." Many young employees also expressed that the benefits made them feel the company’s care. Vice General Manager Deng Cihuo stated that distributing holiday benefits is a long-standing employee care initiative aimed at allowing employees to share in the company’s development achievements and enhancing their sense of belonging and cohesion. In the future, the company will continue to prioritize employee service and support, actively fostering a harmonious and progressive work environment. It is reported that in addition to the physical benefits, the company extended holiday greetings to all employees through notice boards and internal communications, along with safety reminders for holiday travel. The benefits, carrying the company’s blessings, convey sincere gratitude and New Year’s wishes to all employees.

2026年6月23日

2026年6月23日

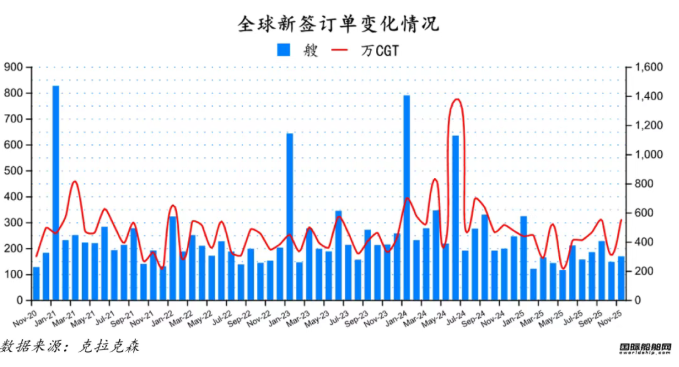

168 vessels! Surge in orders! The latest monthly global shipbuilding report released.

Number of new orders increased by 21 ships month-on-month, Chinese shipyards received the most orders, South Korea ranked second.According to the latest data from Clarksons (as of December 9, 2025), global new orders in November 2025 amounted to 168 ships, totaling 5,528,133 CGT. Compared to global new orders of 147 ships, totaling 3,109,300 CGT in October 2025, the number increased by 21 ships month-on-month, and the compensated gross tonnage rose by 77.79% month-on-month. Compared to global new orders of 198 ships, totaling 5,192,849 CGT in November 2024, the number decreased by 30 ships year-on-year, while the compensated gross tonnage increased by 6.46% year-on-year. In terms of ship types: Bulk carriers: 23 ships, totaling 2,165,100 deadweight tons (DWT). Tankers: 43 ships, totaling 9,871,600 DWT. Chemical tankers: 4 ships, totaling 181,600 DWT. Container ships: 54 ships, totaling 471,280 TEU. Liquefied gas carriers: 3 ships, totaling 365,000 cubic meters. Other ship types: 25 ships, totaling 853,210 CGT. Offshore vessels: 16 ships, totaling 148,660 CGT. In terms of order types: Bulk carriers: 4 Capesize bulk carriers, 10 Panamax bulk carriers, 9 Supramax bulk carriers. Tankers: 24 VLCCs, 7 Suezmax tankers, 10 Aframax tankers, and 2 Panamax tankers. Container ships: 28 Ultra Large Container Ships, 10 Panamax container ships, 7 Sub-Panamax container ships, 6 Handy container ships, and 3 Feeder container ships. From the perspective of shipyard countries:In November, global new ship orders totaled 168 ships, with a combined 5,528,133 CGT. Among these, Chinese shipyards received 113 orders, totaling 2,974,359 CGT; Japanese shipyards received 2 orders, totaling 11,938 CGT; and South Korean shipyards received 40 orders, totaling 1,971,122 CGT. In terms of CGT, they accounted for 53.80%, 0.22%, and 35.66% of global new ship orders, respectively. From January to November 2025, new ship orders totaled 1,957 ships, with a combined deadweight tonnage of 118,966,005 DWT....

2026年6月23日

2026年6月23日

SCFI Rises for Two Consecutive Weeks! Container Shipping Market Defies Off-Season Slump.